Administrative Monetary Fines of the Capital Markets Board in 2025: Prominent Types of Breaches

Introduction

Capital Markets Law No. 6362 (CML) grants the Capital Markets Board (Board) broad administrative sanctioning powers to ensure that capital markets operate in a reliable, transparent, and efficient manner. Among these sanctions, one of the most frequently used instruments is administrative monetary fines, as regulated under Articles 103 and 104 of the CML.

In 2025, within the scope of 68 bulletins[1] it published, the Board imposed administrative monetary fines on 297 real and legal persons; the aggregate amount of these fines reached TRY 2,692,239,472.78 (approximately TRY 2.69 billion). Approximately 79% of this amount stems from fines imposed for market disruptive actions related to orders or transactions, while another significant category of violations consists of breaches of disclosure obligations. Other main types of violations that stood out in 2025 include non-compliance with information systems regulations, violations concerning share sale information forms, breaches of corporate governance principles, and violations of the short-selling ban.

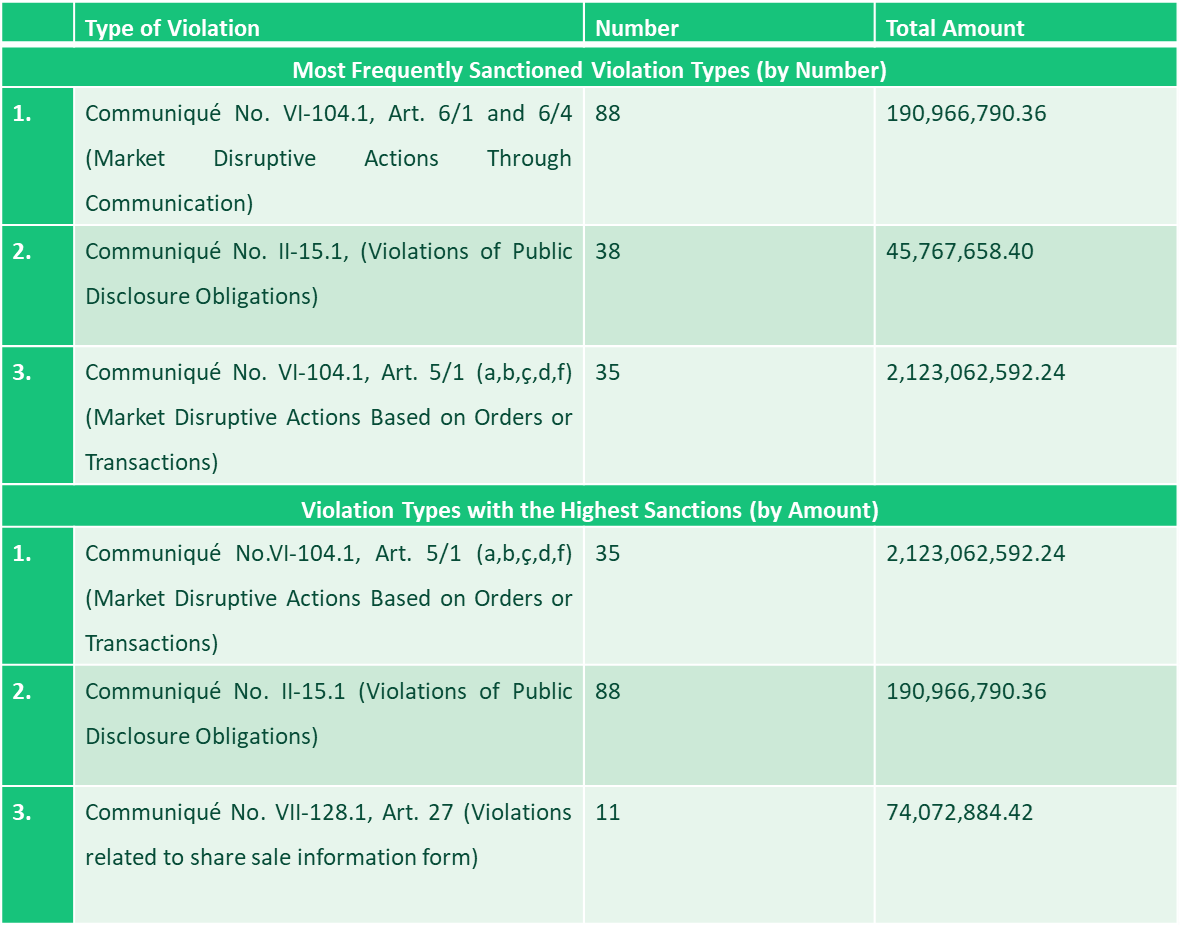

This article examines, within the scope of administrative monetary fines imposed by the Board, market disruptive actions and breaches of disclosure obligations that stand out in terms of both frequency and the magnitude of fines. Comparative data on the types of violations that stood out in 2025 in terms of number and monetary amount are presented in the table below:

Overview of Administrative Monetary Fines under the CML

Pursuant to Article 103 of the CML, the Board is authorized to impose administrative monetary fines on real and legal persons acting in violation of the provisions of the law, the standards and forms determined thereunder, the secondary legislation enacted based on the CML, or the Board’s decisions of a general or specific nature. The minimum and maximum amounts of such fines are determined annually in accordance with the revaluation rate. The CML further stipulates that, in any event where a benefit has been obtained because of non-compliance with an obligation, the administrative monetary fine shall not be less than twice the amount of benefit obtained. In determining the specific amount of the fine, the Board considers the severity of the violation, the status of the offender, and the impact of the act on the market. With respect to administrative monetary fines imposed on legal entities, the applicable fine may be set at up to the higher of 1% of the gross sales revenue or 20% of the profit before tax, as reflected in their most recent independently audited annual financial statements prior to the date of the violation.

Article 104 of the CML provides for a specific regulation concerning market disruptive actions and stipulates that, where a benefit has been obtained through the violation, the administrative monetary fine cannot be less than twice the amount of such benefit.

Within this framework, for an act to qualify as a market disruptive action, (i) it must not be explainable by reference to a reasonable economic or financial rationale, (ii) it must be of a nature that disrupts the confidence, transparency, and stability of stock exchanges and other organized markets, and (iii) the act or transaction in question must not constitute a criminal offence. A benefit need not be obtained for an act to qualify as a market disruptive action; however, where such a benefit exists, it will be considered in determining the amount of the administrative monetary fine.

- Inability to be explained by a reasonable economic or financial rationale: For a transaction or action to be considered a market disruptive action, it must not be justifiable by ordinary investment behavior or rational economic grounds. In this context, it is assessed whether the transactions carried out by the investor are based on reasonable investment justifications such as portfolio management, risk mitigation, fulfillment of collateral obligations, or fundamental/technical analysis. If the transactions cannot be explained by an economic purpose and do not appear consistent with market practices and investor behavior, this criterion will be regarded as satisfied.

- Being of a nature that disrupts the confidence, transparency, and stability of exchanges and other organized markets: The transaction or action must be capable of disrupting the proper functioning of the market, misleading price formation, or creating a false impression regarding supply and demand.

- The act not constituting a criminal offence: Market disruptive actions are regulated as misdemeanors in terms of their legal nature. Therefore, if the relevant act simultaneously constitutes one of the capital markets crimes, criminal law provisions, rather than the provisions on misdemeanors, shall apply.

Market Disruptive Actions: Communiqué No. VI-104.1 on Market Disruptive Actions, Articles 5/1 and 6

The types of market disruptive actions are elaborated in detail under the Communiqué on Market Disruptive Actions No. VI-104.1 (Communiqué No. VI-104.1). Within this framework, “market disruptive actions related to orders or transactions” and “market disruptive actions committed through communication” regulated under Articles 5 and 6 of the Communiqué No. VI-104.1 are examined below.

Market Disruptive Actions Related to Orders and Transactions (Communiqué No. VI-104.1, Article 5/1)

For Article 5/1 of the Communiqué No. VI-104.1 to be applicable, in addition to the elements set out under Article 104 of the CML being satisfied, (i) an act of material or significant effect on the markets must be carried out, and (ii) such act must result in at least one of the following three alternative outcomes: disruption of market confidence, transparency or stability; creation of a misleading impression; or obstruction of fair price formation. Furthermore, it must be demonstrated that the relevant act is the direct cause of such outcome. The misdemeanor may be committed by a single person or by persons acting in concert.

The most common types of violations under Article 5/1 are summarized below. These acts qualify as market disruptive actions where the above-mentioned elements are present:

- Subparagraph (a) – Buying/selling, account movements, order submission/cancellation/amendment: These are the core market actions covering the entire process from the submission of an order to the completion of settlement. Order submission refers to buy/sell instructions communicated by investors to investment firms, whether in writing or orally; order cancellation refers to the withdrawal of an order that has not yet been executed; and order amendment refers to the modification of elements such as price or quantity of an order that has not yet been executed, within the framework of Article 29/2 of the Borsa İstanbul Inc. Regulation on the Principles of Exchange Activities.

- Subparagraph (b) – Submission of orders at different price levels: This act involves placing orders simultaneously or consecutively at different price levels for the same capital markets instrument.

- Subparagraph (ç) – Self-trading or matched orders (wash trades): Self-trading refers to fictitious transactions carried out by a person acting as both buyer and seller between their own accounts, which do not result in any genuine change in ownership of the capital markets instrument[2]. In supervisory reviews, the short time intervals between the submission of orders are considered an important indicator that the transactions lack a reasonable economic rationale and are carried out with the intent to disrupt the market[3]. Such actions are deemed market disruptive due to their capacity to create artificial trading volume and price appearance, thereby misleading third parties.

- Subparagraph (d) – Transactions aimed at influencing opening or closing prices: This includes practices such as order stacking (layering) at the end of a session or artificially altering the closing price through small-volume orders, typically with the aim of reversing the price the following day to generate profit.

- Subparagraph (f) – Transactions aimed at increasing, decreasing, or stabilizing prices: These involve attempts to artificially push prices upward or downward, or to maintain them at a certain level, by placing buy orders above or sell orders below the prevailing market price.

In 2025, fines imposed under Article 5/1 of the Communiqué No. VI-104.1 ranked third in terms of number, with 35 separate violations, and ranked first in terms of total monetary amount, reaching TRY 2,123,062,592.24. This amount corresponds to approximately 78.9% of the total administrative monetary fines imposed in 2025. The highest fine imposed on a single real or legal person within this category amounted to TRY 362,123,139.86.

Market Disruptive Actions Committed Through Communication (Communiqué No. VI-104.1, Articles 6/1 and 6/4)

Under Article 6/1 of Communiqué No. VI-104.1, providing false, incorrect, or misleading information, spreading rumors, publishing news, making disclosures of material events, issuing comments, or preparing reports that may affect the price or value of capital markets instruments or investors’ decisions are deemed market disruptive actions.

However, following a legislative amendment introduced in 2017, the qualification of such acts as market disruptive actions has been made subject to an additional requirement. Accordingly, the mere creation or dissemination of false or misleading information is not considered sufficient; it is also required that the persons engaging in such acts have placed orders or executed transactions in the relevant capital markets instrument before or after such conduct. In other words, the conduct aimed at influencing the market through misleading information must be linked to the offender’s transactions in the relevant capital markets instrument.

Article 6/4 of the Communiqué No. VI-104.1 further defines as a market disruptive action the conduct of persons who, through mass media such as newspapers, television, the internet, or similar channels, provide commentary or investment recommendations on capital markets instruments, and then engage in transactions contrary to such recommendations before revising them or, in any event, within five business days. Accordingly, for instance, where a person who issues a buy or hold recommendation for a capital markets instrument executes a sale within this period, or where a person who issues a sell recommendation subsequently carries out a purchase, such conduct falls within this scope.

The primary objective of this regulation is to prevent individuals from directing investors in a particular direction through mass media and subsequently obtaining unfair gains by taking contrary positions, thereby safeguarding investor confidence in the capital markets.

According to the data for 2025, violations under Articles 6/1 and 6/4 of Communiqué No. VI-104.1 constitute the most frequently sanctioned type of violation, with 88 individual fines imposed. The total amount of administrative monetary fines imposed for these violations reached TRY 190,966,790.36. The highest individual fine imposed on a single real or legal person within this category amounted to TRY 16,973,240.42 and was imposed in relation to a social media-driven buy-sell manipulation scheme.

Breaches of Disclosure Obligations

The Communiqué on Material Disclosures No. II-15.1 (Communiqué No. II-15.1) requires publicly traded companies and capital markets institutions to disclose, fully and without delay, all information that may affect investors' investment decisions, to be disclosed on the Public Disclosure Platform (PDP). Through this regulation, it is accepted that information asymmetry is reduced, thereby facilitating the efficient functioning of the markets[4].

The main provisions of the Communiqué that are most frequently subject to violations are summarized below:

- Disclosure of Inside Information (Art. 5): For the disclosure obligation to arise under this article, the information to be disclosed must qualify as “inside information”, meaning information that has not yet been publicly disclosed, relates to a specific financial instrument, and is of a nature that could influence a reasonable investor’s investment decision. Such information includes facts, events, and developments that may provide an advantage to those possessing the information over other investors and that may affect the value, price, or investors’ decisions once disclosed to the public[5]. The fact that the information has not yet become definitive does not, in and of itself, extinguish the disclosure obligation. However, for the obligation to arise, the information must relate to existing conditions or events, or to those that may reasonably be expected to occur and must be sufficiently specific to enable an assessment of their potential impact on the value, price, or investors’ decisions regarding the relevant capital markets instrument.

- Transaction Notifications (Art. 11): Pursuant to this article, persons discharging managerial responsibilities, persons closely associated with them, and the controlling shareholder of the issuer are required to publicly disclose their transactions in the issuer’s shares and capital markets instruments based on such shares. However, no disclosure is required unless the total amount of transactions carried out within a calendar year reaches TRY 12,000,000[6](applicable for 2025). Once this threshold is exceeded, all transactions conducted from the transaction by which the threshold was exceeded must be disclosed. The same rule applies to transactions in capital markets instruments other than the issuer’s publicly offered shares.

- Timely and Complete Disclosure (Art. 23): This provision requires that, where a material development occurs, it must be disclosed to the public immediately (Art. 23/2), and that disclosures must be updated where a new development arises that affects the content of a previously made disclosure (Art. 23/7). Information regarding changes in capital or management control must be disclosed by the morning of the third business day following the occurrence of such change. Disclosures must be made using the relevant forms available on the PDP.

- Nature of the Disclosure (Art. 24): This article requires that public disclosures be complete, clear, and not misleading to investors. Article 24/3 explicitly prohibits misleading disclosures and covers not only statements containing false information, but also those that, while factually accurate, create an overall misleading impression due to being incomplete or selectively presented. Given that levels of financial literacy may vary among investors, the standard to be applied in assessing the clarity and adequacy of disclosures should be that of the average investor[7].

In 2025, violations under Communiqué No. II-15.1 ranked second in terms of frequency, with 38 individual fines and a total amount of TRY 45,767,658.40. The highest individual fine imposed on a single natural or legal person within this category amounted to TRY 5,833,734.00. It is noteworthy that, in 2025, violations were not limited to delayed disclosures, but that misleading disclosures in terms of content were also frequently subject to sanctions.

Conclusion

The data for 2025 clearly reveals the priorities underlying the Board’s administrative enforcement policy: the fact that approximately 79% of the administrative monetary fines—exceeding TRY 2.69 billion in total—stem solely from market disruptive actions related to orders or transactions demonstrates the intensity of supervision in this area and the Board’s strong commitment to deterrence. On the other hand, market disruptive actions committed through communication, as well as breaches of disclosure obligations, stand out as the most frequently sanctioned types of violations in terms of the number of fines imposed.

Real and legal persons subject to administrative monetary fines may, following the notification of the decision, first seek administrative review before the Board and subsequently initiate an annulment action. For capital markets participants, strengthening compliance frameworks and ensuring the effective operation of internal control mechanisms has become an indispensable requirement not only for preventing financial losses but also for safeguarding corporate reputation.

- The Board’s 2025 Bulletins: https://spk.gov.tr/spk-bultenleri/2025-yili-spk-bultenleri?s=1.

- Communiqué No. VI-104.1 on Market Disruptive Actions, Article 3(1)(g)

- Tok, Ahmet: Sermaye Piyasası Hukukunda Piyasa Bozucu Eylemler, İstanbul, 2023, p. 150.

- Memiş, Tekin / Turan, Gökçen: Sermaye Piyasası Hukuku, Ankara 2022, p. 49.

- Board, Guide on Material Disclosures, p. 4.

- As of 2026, the relevant amount has been set at TRY 15,000,000.

- Gürler, E. Hazal: Hukuki Açıdan Sermaye Piyasasında Özel Durum Açıklamaları, İstanbul, 2023, p. 168.

All rights of this article are reserved. This article may not be used, reproduced, copied, published, distributed, or otherwise disseminated without quotation or Erdem & Erdem Law Firm's written consent. Any content created without citing the resource or Erdem & Erdem Law Firm’s written consent is regularly tracked, and legal action will be taken in case of violation.

Other Contents

Real estate investment companies (“REICs”) are among the most significant capital markets institutions in Türkiye, bridging the capital markets and the real estate sector. Through REICs, investors gain access to real estate markets and the opportunity to generate returns from this sector without directly acquiring property…

In its most basic form, securitization is the process of pooling and repackaging illiquid assets or rights with the purpose of converting them into tradable and interest-bearing financial instruments to be issued to capital market investors…

The reduction of the share capital is a transaction that results in the nominal decrease of the share capital item on the balance sheet. The nature of a share capital reduction is an amendment to the articles of association. Articles 473–475 of the Turkish Commercial Code No. 6102 (“TCC”) regulate the general principles of capital reduction.

A new legislative package, the Listing Act, was adopted by the European Council on October 8, 2024 to make capital markets within the European Union (“EU”) more attractive and facilitate companies' IPO process. The Listing Act amends the EU Prospectus Regulation, the EU Market Abuse Regulation, the Markets...

Crypto assets have become a significant component of financial markets in recent years, prompting the development of a regulatory framework in response to growing investor interest. In this context, both the amendments to Capital Markets Law No. 6362 (“CML”) and various resolutions issued by the Capital...

New ventures and, in this context, start-up companies have been essential players in economic life for a long time. Significantly in terms of new technologies and creative ideas, instead of established and large structures, new ventures and structures where individuals' personal contributions matter more greatly...

The website is one of the most important tools that reinforces the transparent management approach of companies and enables company stakeholders such as shareholders, company creditors, and those who carry out activities with the company to access important information about the company quickly and...

Crypto assets have created a significant change in the financial system with the emergence of blockchain technology. The decentralized and digital nature of these assets has offered a new method outside of traditional monetary systems...

The Keener decision represents a pivotal moment in interpreting and applying securities laws as it pertains to the definition and regulatory treatment of “dealers” within financial markets.This case arose from actions taken by the Securities and Exchange Commission (“SEC”) against Justin W. Keener, who was accused...

Responsible Management Principles (Stewardship Principles, SP) have been regulated by the Capital Markets Board (CMB) regarding the securities investment funds (Funds) founded by Portfolio Management Companies (PMC)...

Information holds paramount importance in the capital markets. Investors, whether seasoned professionals or newcomers, depend on various sources to guide their decisions amidst the complexities of the capital markets...

In the intricate web of finance and law, the US Court of Appeals for the Second Circuit’s ruling of Kirschner v. JP Morgan Chase Bank, N.A. (“Kirschner Ruling”) stands at the confluence of international banking regulations and securities law, presenting a thorough examination of the legal frameworks governing the...

Sustainability-linked derivatives transactions involve the embedding of a cash flow in derivatives that will change in a sustainability-linked way, and institutions' compliance with environmental, social, and governance (ESG) objectives is monitored using specific performance indicators...

There is no specific procedure in the Turkish Commercial Code (TCC) that publicly traded corporations must follow in terms of providing collaterals, pledges, mortgages and sureties (CPMS). Authority for and procedure of provision of CPMS are determined according to the general rules...

In line with the financing needs of companies and their desire for institutionalization, the number of public offerings shows an upward trend across Türkiye. Looking at the data published by the Capital Markets Board on its website regarding initial public offerings, it is seen that, it is seen that 35 public offerings...

The Communiqué on the Principles Regarding the Companies whose Shares will be Traded on the Venture Capital Market (II-16.3) ("Communiqué") has facilitated for private joint stock companies to sell their shares to qualified investors without a public offering. Thus, a new opportunity is created for joint stock...

Swiss Financial Markets Supervisory Authority (“FINMA”), through its decision dated 19 March 2023, approved the merger of Credit Suisse with UBS Group AG (“UBS”) and to write down the Additional Tier 1 capital bonds (referred to as AT1) issued by Credit Suisse, with a total value of approximately CHF 17 billion...

The Capital Markets Board’s (“Board”) long-awaited Communiqué on Crowdfunding No. III - 35/A.2 (“Communiqué”) entered into force through its publication in the Official Gazette numbered 31641 and dated 27 October 2021...

Mortgage covered bonds are one of today’s most common structured finance products. Although they have a prominent presence in the marketplace today, these bonds have historical roots in the Pfandbrief of 18th century Prussia. In the aftermath of the Seven Years War, King Frederick the Great implemented...